Executive Summary

For many solo attorneys, bookkeeping problems do not appear overnight. They build quietly in the background, one miscategorized transaction, one failed sync, one unreconciled month at a time, until tax season exposes the full extent of the damage.

This case study follows a solo litigation attorney whose QuickBooks Online file had become functionally unusable just 45 days before the federal tax filing deadline. Over a 14-month period, automated bank rules, improperly configured integrations, and inconsistent trust accounting procedures created widespread ledger inaccuracies across operating accounts, trust liabilities, and reimbursable client expenses.

The situation had escalated beyond routine bookkeeping cleanup. The attorney was facing:

- Unreconciled bank accounts

- Duplicate invoices

- Broken trust in accounting records

- Distorted profit and loss reporting

- Potential compliance exposure

- Mounting tax-season pressure

Within less than 30 days, the entire accounting infrastructure was reconstructed, reconciled, and converted into a tax-ready, audit-supportable financial system.

The final outcome included:

- 14 months of cleaned and reconciled financial records

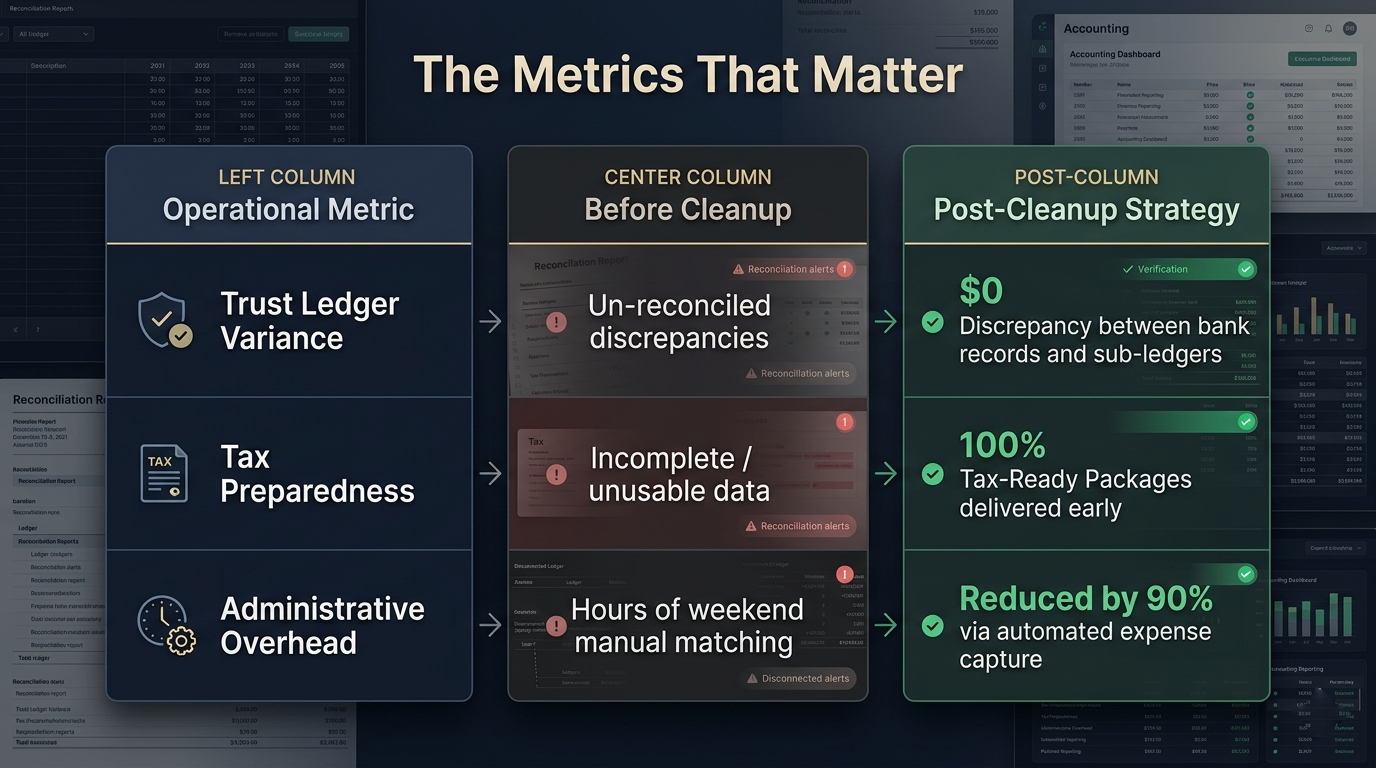

- $0 discrepancy between bank balances, trust liabilities, and client ledgers

- Fully restructured legal-specific Chart of Accounts

- Tax-ready reporting delivered before filing deadlines

- Operational workflows designed to prevent future data corruption

About the Author

This case study was prepared by a Certified QuickBooks ProAdvisor specializing in legal bookkeeping systems, trust accounting workflows, and financial cleanup projects for solo attorneys and small law firms using QuickBooks Online.

Why Standard Bookkeeping Methods Failed

Standard retail or SaaS bookkeeping models operate under a single-source revenue framework. They routinely fail in a legal environment because they do not account for the absolute separation of operational capital and unearned client trust balances. In this case, a generalist accounting service applied standard business automated banking rules within QBO , which automatically categorized complex legal transfers without evaluating true matter-level account distribution.

Specific Diagnostic Symptoms Identified:

- Commingling of Funds via Processing Fees: When clients paid invoices via electronic credit card processing, merchant processing fees were automatically deducted directly from the incoming trust deposits rather than being routed out of the operating bank account. This altered the physical balances of client trust funds.

- Automated Sync Overrides: The unattended LPMS integration continuously generated duplicate invoices and unmapped payments across both platforms. This introduced massive layers of phantom revenue that artificially inflated the firm’s profitability on paper.

- Negative Asset and Balance Sheet Distortions: Unposted deposits and misclassified client sub-accounts created negative liability balances, turning the balance sheet into an unusable roadmap for tax preparation.

The Agitation: The Hidden Cost of Financial Blind Spots

Operating an expanding legal practice with corrupted ledger records introduces severe, compounding risks that impact both professional licensing and bottom-line profitability.

1. Severe Compliance & Tax Risks

With tax season rapidly approaching, the attorney faced a high risk of filing inaccurate profit and loss metrics. This exposed the business to potential IRS audit penalties and significant tax overpayments driven by duplicated, artificial revenue entries. Even more critical was the existential risk of non-compliant trust records. Inadvertent trust accounting errors—such as un-tracked individual client balances—can trigger immediate State Bar inquiries, threatening an attorney’s license to practice law.

2. The Operational Bottleneck & Cash Flow Strain

The attorney was spending un-billable weekend hours manually cross-checking client statements instead of focusing on high-value, revenue-generating client matters. Furthermore, because the generic account layout didn’t separate advanced client costs from general overhead expenses, thousands of dollars in reimbursable court costs, filing fees, and deposition expenses were slipping through the cracks unnoticed. The firm was inadvertently financing client litigation out of its own operating capital, creating severe operational cash flow strains.

The Solution (Part 1): Technical Workflow & Reconstruction Strategy

Resolving 14 months of deep financial data corruption required a multi-phase forensic accounting strategy implemented directly inside QuickBooks Online.

Step 1: The Integration Break and Ledger Freeze

To permanently halt the data corruption, the active database sync between the LPMS billing system and QuickBooks Online was completely disconnected. This froze the historical records. Next, a definitive data baseline was established by pulling physical bank and credit card statements for the entire 14-month period, creating an immutable control ledger to audit against the internal QBO registers.

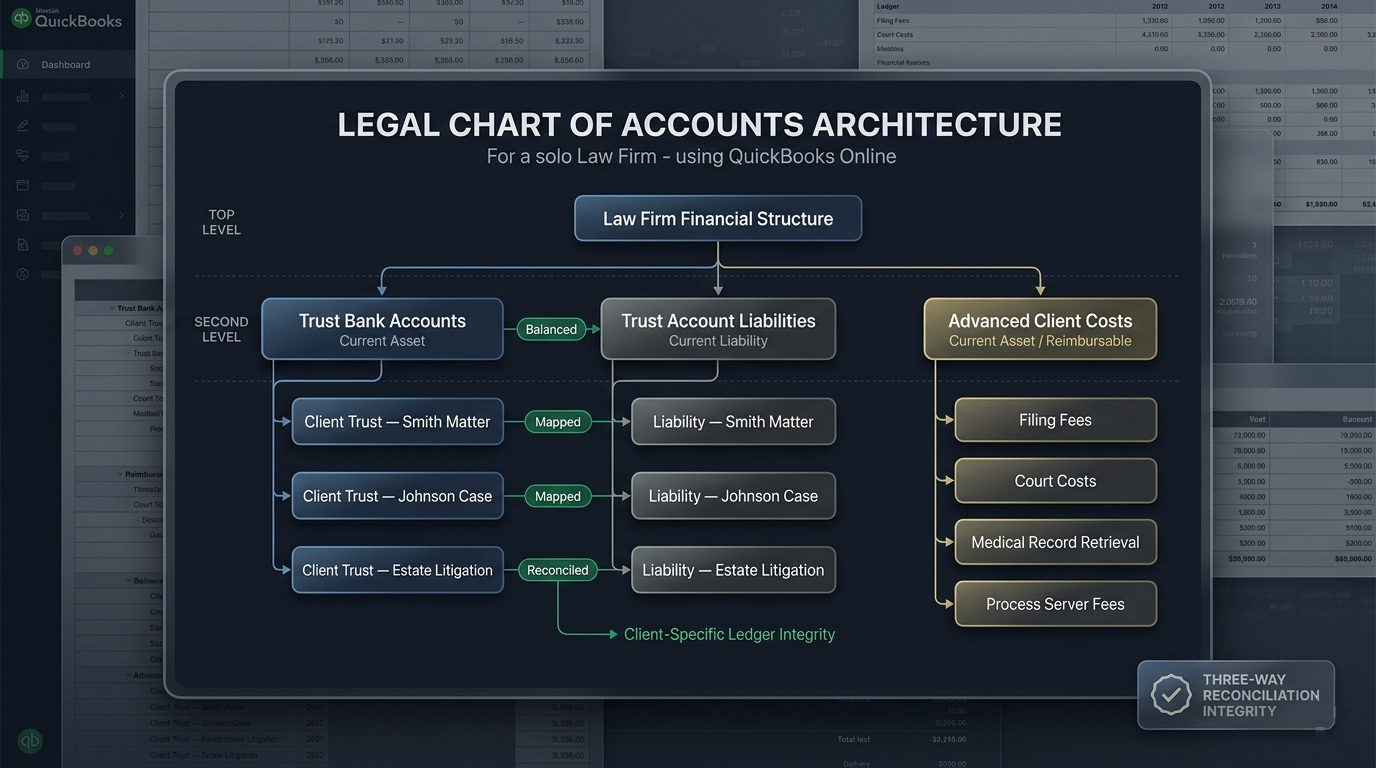

Step 2: Architecture Overhaul (The Legal Chart of Accounts)

The generic Chart of Accounts was overhauled and replaced with a specialized framework tailored for solo law firms. This required mapping distinct balances across three core long-term account layers:

By ensuring that every individual client matter was mapped to both a Trust Asset account and a corresponding Trust Liability sub-ledger, we guaranteed that trust balances remained perfectly self-contained.

Step 3: Forensic Transaction Matching & De-Duplication

Using specialized QuickBooks clean-up utilities, the forensic cleanup followed a precise technical sequence:

- Purging Duplicate Items: Using the Reclassify Transactions tool, hundreds of phantom entries and duplicate automated invoices generated by the faulty sync were isolated, batched, and systematically purged from the system.

- Isolating Merchant Fees: Every credit card processing transaction over the 14-month period was evaluated. Deducted processing fees were unbundled from trust transfers, tracked, and reconciled by shifting the fee obligations back to the operational bank account where they legally belonged.

- Parent-Subaccount Reconciliation: Every single unidentified trust transaction was traced to its physical origin and mapped to specific client sub-ledgers, establishing clear accounting paths for each matter.

The Solution (Part 2): The Human Element & Structural Accountability

Technology alone cannot solve complex systemic accounting breakdowns; sustainable recovery requires human advisory, intentional workflow design, and professional support.

Alleviating Administrative Paralysis

When an administrative backlog grows large enough, it induces a state of operational paralysis. Part of our diagnostic implementation involved managing this immense emotional weight, moving the attorney out of crisis-management mode and establishing clear structural transparency.

Designing the Post-Cleanup Framework

To prevent a recurrence of ledger corruption, we implemented simple, sustainable daily and monthly administrative operational frameworks:

- Daily Material Expenses Capture: A streamlined daily workflow was deployed using custom QBO product/service items mapped directly to the Advanced Client Costs asset account. When vendor checks or filing fees are generated, the attorney quickly tags the specific client matter, instantly staging that billable cost for the next invoice cycle.

- Rigid Closing-Date Hard Locks: We established monthly closing-date safeguards in QBO protected by administrative credentials. This locks historical, closed months completely, preventing any future manual user modifications, bank feed overrides, or software sync updates from altering verified data.

The Results: Measurable Cleanliness & Business Optimization

By deploying a focused, specialized approach, the entire 14-month backlog was completely audited and transformed into a powerful business tool within 25 days.

From the Courtroom: Client Perspective

“Walking into tax season with an un-reconciled trust account was an incredibly stressful weight. Having a specialist break down the errors, isolate the data duplicate patterns, and present a flawless, audit-proof three-way reconciliation report provided absolute peace of mind. I can finally refocus entirely on my clients and billable hours.”

Is Your Firm Tax-Ready and State Bar Compliant?

QuickBooks Online is a highly capable accounting engine for modern law firms, but it requires precise, specialized structural architecture to maintain strict compliance and stop financial leakage. If your firm relies on standard automation workflows or generalist accounting methods, hidden errors may be compromising your compliance.

Don’t wait for an tax deadline or a compliance notification to address your books.