It is Sunday night at 8:30 PM. While the rest of the household is winding down, a solo law firm owner sits at their kitchen table, staring at QuickBooks Online (QBO). They clear the final transaction from the bank feed, hit “Reconcile,” and wait for the software’s feedback. A moment later, the screen flashes a satisfying green checkmark. The bank statement and QBO match perfectly down to the penny.

The attorney closes their laptop, feeling a temporary sense of relief. The books are “done” for the month.

The Core Paradox

But this relief is built on a dangerous illusion. While the bank account and the accounting software reconcile flawlessly with each other, a compliance time bomb is quietly ticking in the background.

The attorney recently cross-referenced their internal case management software and practice ledgers, only to find a glaring discrepancy. The grand total of what they owe their clients on paper does not match the actual cash sitting in the Interest on Lawyers’ Trust Accounts (IOLTA).

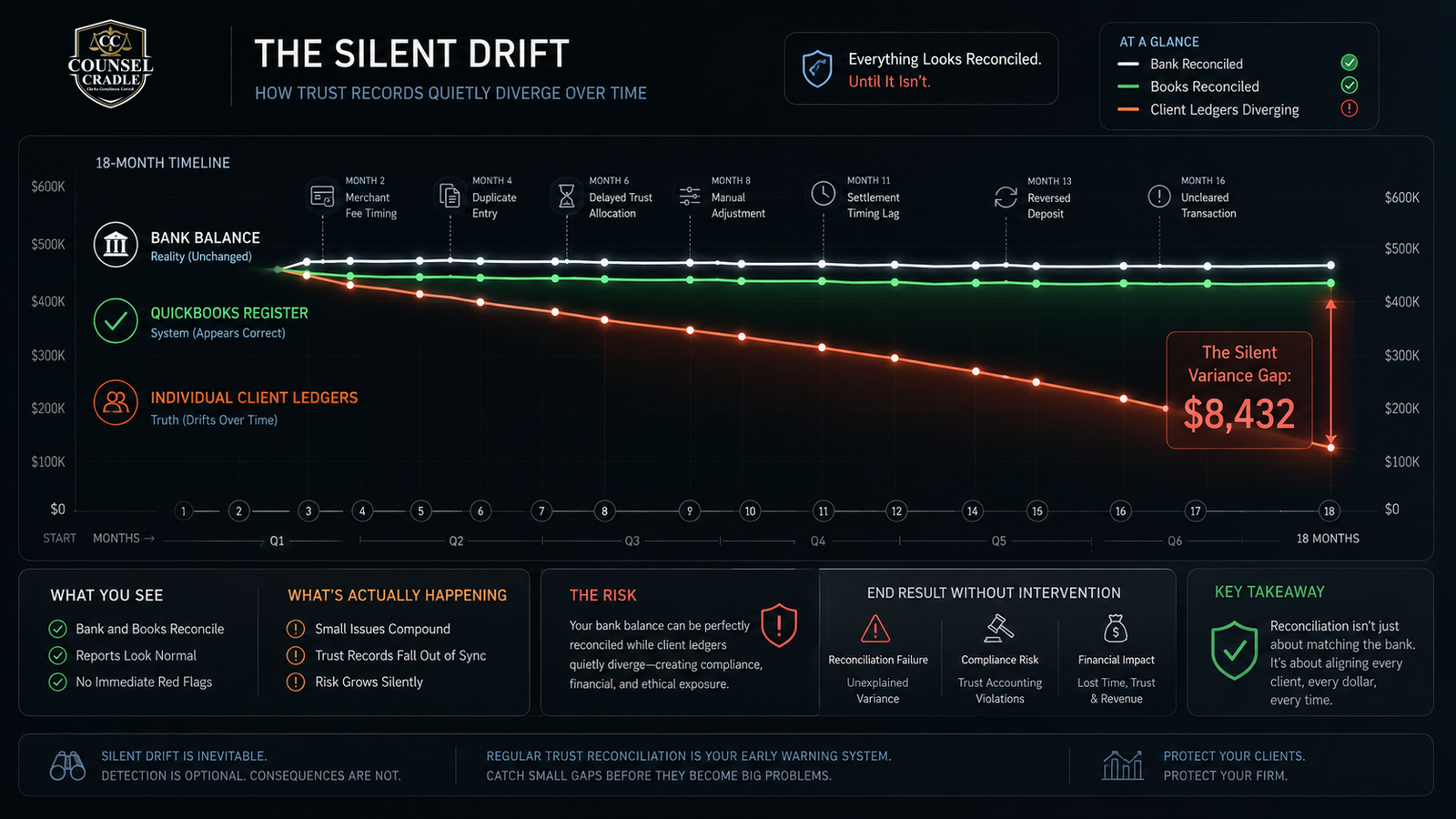

The Paradox: A perfect two-way bank reconciliation does not mean your law firm is compliant. It simply means your accounting software agrees with your bank. It says absolutely nothing about whether your individual client ledgers match reality.

In this specific case, an initial $8,432 silent variance had accumulated unnoticed over 18 months. Below is a high-level summary of the transformation achieved once the underlying drift was isolated, diagnosed, and resolved:

Performance Metrics At-A-Glance

- Trust Ledger Variance Cleared: From $8,432.00 down to exactly $0.00.

- Trapped Revenue Unlocked: $4,200.00 in stagnant, earned fees safely identified and transferred to the operating account.

- Time Returned to Owner: 8 hours of monthly weekend administrative stress eliminated.

2. The Problem: The Weekend Bookkeeping Habit That Created the Drift

For most solo attorneys, weekdays are swallowed whole by client consultations, court appearances, depositions, and brief writing. Bookkeeping naturally gets relegated to bulk weekend sessions. While disciplined, this weekend ritual often introduces systemic errors due to the unique nature of legal trust accounting.

Standard general business accounting methodologies fail when applied to law firms. QuickBooks Online is built as a general business tool; its native reconciliation protocol checks only the bank statement against the QBO bank register. This is a standard two-way reconciliation. QBO does not natively mandate, force, or automate a reconciliation against the individual client ledgers housed inside external billing platforms or manual spreadsheets.

Over an 18-month period, several minor, seemingly harmless factors combined to create a major compliance blind spot:

- Merchant Integration & Timing Lags: The firm utilized card processors like LawPay or Clio Payments. When a client paid a retainer on a Friday afternoon, the processor batched the transaction, but the cash didn’t physically settle in the IOLTA until Tuesday. The attorney, recording transactions during weekend sessions, manually logged the revenue on Sunday, creating an artificial timing discrepancy.

- Unrecorded Bank & Wire Fees: Occasional wire fees or merchant processing fees were inadvertently deducted directly from the trust account rather than the operating account, causing a silent drop in the pooled balance without a corresponding change in any single client ledger.

- Inconsistent Fee Transfers: When flat fees or hourly retainers were earned, the attorney transferred lump sums from trust to operating based on memory or rough calculations, rather than matching exact invoice lines.

- Duplicate and Manual Entries: To force the green “reconciled” checkmark in QBO on Sunday nights, the attorney occasionally made manual adjustments or accepted duplicate entries suggested by automated bank feeds, masking underlying structural errors.

3. The Agitation: Why This Becomes Dangerous Quickly

The turning point occurred when the attorney prepared to refund a client whose matter had concluded. When checking the client’s ledger in their billing software, the balance stated $2,500. However, a deep review of the pooled trust account revealed that if they wrote that check, the total cash remaining would drop below the collective balances owed to the rest of the firm’s active clients.

They had hit the terrifying realization that what they owed clients on paper did not match the cash sitting in the bank.

The mathematical discrepancy translates directly into severe real-world liabilities:

Real-World Risks & Consequences

- Potential Commingling: If you unknowingly overdraw one client’s funds to pay another—even by a few hundred dollars because of a timing lag—you are technically committing commingling. This is the fastest track to a State Bar disciplinary action or disbarment. State Bar rules demand zero variance.

- Financial Paralysis: Out of sheer terror of accidentally overdrawing the trust account, the attorney stopped transferring earned fees out of the IOLTA altogether. This left $4,200 in hard-earned, legitimate firm revenue completely trapped, severely choking the firm’s operational cash flow.

- The Loss of Personal Freedom: Weekends were no longer restful. Instead, they were consumed by manual, frustrating spreadsheet triangulation, trying to find tiny discrepancies across hundreds of historical entries, searching for a needle in a haystack.

4. The Real Issue

The problem wasn’t a failure of QuickBooks Online, Clio, or LawPay. Rather, it was the application of general business bookkeeping habits to a highly regulated legal trust environment.

A standard business owner cares primarily about cash flow and matching bank statements to software registers. A lawyer must treat every single dollar in the trust account as an independent liability owed to a specific human being or entity. When bulk weekend data entry meets automated sync integrations without trust-specific controls, a drift between the bank and the client ledgers is virtually inevitable.

5. The Solution: Three-Way Reconciliation Workflow

To resolve the $8,432 variance, we deployed a systematic, forensic three-way triangulation workflow. This process moves beyond standard accounting to align three completely independent data silos.

Phase 1: Diagnosis & Data Collection

- Establish a Hard Ledger Freeze: All new manual data entry, retroactive edits, and fee transfers were temporarily paused to ensure a static testing environment.

- Dataset Extraction: We pulled three distinct reports mapped strictly to the same cutoff date (e.g., October 31):

- The formal IOLTA bank statement ending balance.

- The QuickBooks Online General Ledger report for the Trust Liability account.

- The Summary of Individual Client Ledgers extracted from the legal billing software.

Phase 2: Forensic Cleanup & Discrepancy Isolation

- Audit the “Trust Liability by Client” Report: We analyzed the historical ledger inside QBO to verify that every deposit and withdrawal was mapped to a specific client sub-account, rather than dumped into a generic pooled bucket.

- Identify Check & Deposit Timing Skews: We cross-referenced outstanding checks. We discovered three historical checks that had been mistakenly marked as “cleared” during a weekend bulk-matching session in QBO but had not actually been cashed by the recipients.

- Correct the Merchant Sync Flaw: We investigated the integration between the credit card processor and QBO. The integration was pushing gross processing deposits to the bank register but failed to automatically log the processing fees into the operating account, leaving a trailing variance every time a client paid via credit card.

- Rebuild Individual Balances: Step-by-step, we adjusted the unrecorded fees, corrected the artificial timing lags, and updated the true balances of each individual client matter.

Phase 3: True Three-Way Reconciliation Protocol

We verified compliance by executing the core legal accounting equation:

$$\text{Bank Statement Balance} = \text{QBO General Ledger Trust Balance} = \sum(\text{Individual Client Ledgers})$$

To demonstrate how the three-way ledger aligns numbers clearly, review this structural model:

| Component | Target Balance | Status |

|---|---|---|

| 1. Cleared Bank Statement Balance | $52,150.00 | Verified |

| 2. QuickBooks Online Trust Liability Register | $52,150.00 | Reconciled |

| 3. Sum of All Individual Client Ledgers | $52,150.00 | Balanced |

| Three-Way Variance | $0.00 | Compliant |

Phase 4: Hardcoding Compliance for the Future

To ensure this drift never happens again, we built permanent operational guardrails:

- Chart of Accounts Restructuring: We mapped the QBO Chart of Accounts into a strict parent-child structure where the primary IOLTA Asset account mirrors the primary Trust Liability account, completely eliminating the use of manual journal entries that cause data skews.

- Weekly Mini-Reconciliation Cadence: Shifting from monthly bulk weekend sessions to a structured, 15-minute weekly verification process minimized the impact of timing lags.

- The Audit Packet Generation: At the close of every month, the firm now automatically generates and archives a single, validated “Three-Way Reconciliation PDF Packet”. This packet contains the bank statement, the QBO reconciliation report, and the client ledger summary, creating an ironclad audit trail for the State Bar.

6. The Results & Transformation

By dismantling the casual weekend bookkeeping habit and substituting a rigorous three-way control framework, the firm experienced an immediate operational and financial turnaround:

- The Mathematical Resolution: The $8,432 discrepancy was entirely resolved, bringing the three-way variance to a perfect $0.00. Every penny in the bank account was successfully mapped to its rightful owner.

- Unlocked Cash Flow: During the forensic cleanup, we identified $4,200 in historic hourly work that had been successfully billed and earned but never transferred out of the trust account due to the attorney’s fear of overdrawing. This cash was immediately and safely moved to the firm’s operating account.

- Time & Lifestyle ROI: The attorney’s monthly administrative commitment dropped from 8 hours of stressful weekend guesswork to 0 hours of trust bookkeeping, completely offloading the compliance risk.

- Emotional Win: The low-grade, constant background anxiety regarding a potential surprise State Bar audit was replaced with total confidence in the structural clarity of the firm’s financials.

7. The Human Element & Expert Insight

The core limitation of modern legal tech is that software integrations alone cannot force compliance. Software is only as reliable as the workflow managing it. Solo attorneys are uniquely vulnerable to trust account issues not because they lack financial integrity, but because they lack the time, specialized accounting training, and objective professional oversight required to manage a dual-entry ledger system.

When a solo attorney transitions away from playing the role of an unqualified weekend bookkeeper, they protect their law license and reclaim their identity as a high-earning legal strategist. True business scale happens when the owner stops trying to solve complex compliance puzzles on Sunday nights and instead implements systems designed by experts.

8. FAQ Section

What is a three-way trust reconciliation?

A three-way trust reconciliation is a specialized accounting workflow mandatory for law firms. It requires checking that three distinct records match exactly on any given date: the cleared IOLTA bank statement balance, the QuickBooks Online trust liability general ledger balance, and the exact sum of all individual client ledger balances combined.

Why doesn’t my trust balance match QuickBooks even when the bank reconciles?

This occurs because standard QuickBooks reconciliation is only a two-way check. It ensures your bank feed matches your QBO bank register, but it does not check your individual client ledgers. Timing lags from credit card processors, unrecorded merchant fees, or manual ledger adjustments can easily cause your client ledgers to drift away from the bank balance, creating a hidden, silent variance.

How often should law firms reconcile trust accounts?

While most State Bars legally mandate a three-way reconciliation on a monthly basis, it is highly recommended for solo practitioners to perform a basic check weekly. This prevents small integration sync errors or timing discrepancies from compounding into massive forensic cleanups over time.

Can trust errors happen even if the bank balance matches?

Yes, absolutely. This is the core danger of the “perfect bank rec”. Your bank account and QuickBooks can balance perfectly down to the penny while you simultaneously have an unrecorded $8,000 variance across your individual client accounts, leaving you entirely out of compliance with state guidelines.

What causes client ledger discrepancies?

The most common causes include merchant processing fee deductions from the wrong account, timing delays during weekend data entry, double-depositing bank feeds, and failing to create individual client-matter sub-accounts within your primary Chart of Accounts.

9. Conclusion & Call to Action

The vast majority of legal trust account disasters do not start with intentional fraud; they start with innocent, repeated bookkeeping habits performed by tired business owners on the weekends. A matching bank balance in QuickBooks Online is simply not enough to guarantee your license is safe. Solo law firms require a precise, dedicated three-way legal bookkeeping workflow to establish true regulatory compliance.

Is your weekend bookkeeping routine hiding a silent variance? Don’t wait for a surprise State Bar audit to find out if your client ledgers match perfectly. Contact us today to schedule a complimentary Trust Account Diagnostic Review, and let us ensure your books are completely bulletproof.

Front Matter / Metadata For SEO

- Target Persona: Busy solo law firm owner who manages their own weekend bookkeeping in QuickBooks Online (QBO) while using separate internal billing software or spreadsheets.

- Primary Focus Keyword: three-way reconciliation, QuickBooks Online law firm

- Secondary Keywords: trust reconciliation for law firms, three-way trust reconciliation, legal trust account reconciliation, solo attorney bookkeeping, trust ledger variance cleanup for lawyers

- Meta Description: Your QuickBooks bank balance matches perfectly, but client ledgers don’t? Discover how a common weekend bookkeeping habit created an $8,432 silent trust variance and the exact three-way reconciliation system that fixed it completely.